Retail investing in the future will look very different from retail investing in the past

In the past 18 months, the retail investing landscape has changed drastically. Not only have the trading apps across the globe seen volumes surge, but the asset classes that retail investors are choosing to invest in have changed drastically. Today’s retail investors are more interested in investing across assets like equity, options, crypto, and NFT as opposed to the previous generation of investors that were interested in gold, real estate, and fixed deposits.

One may argue that these preferences are emblematic of the broader euphoria that exists around the equity market and the bull run we have been on for the past 12+ years all of which make for a bubble. However, retail investors today have more information, accessibility, and tools than ever before to make or take advice for their investment decisions.

Having said this, let’s look at the retail investing landscape in India, how the brokerage industry has grown in the past 18 months, monetization pools have evolved, AMC licenses and passive funds have become attractive and the rise of alternative investments for retail investors.

Indian investors prefer physical assets over financial assets

Each person behaves in a different way when it comes to investing their money, some prefer financial assets while some prefer physical assets, some prefer safe bets while others riskier.

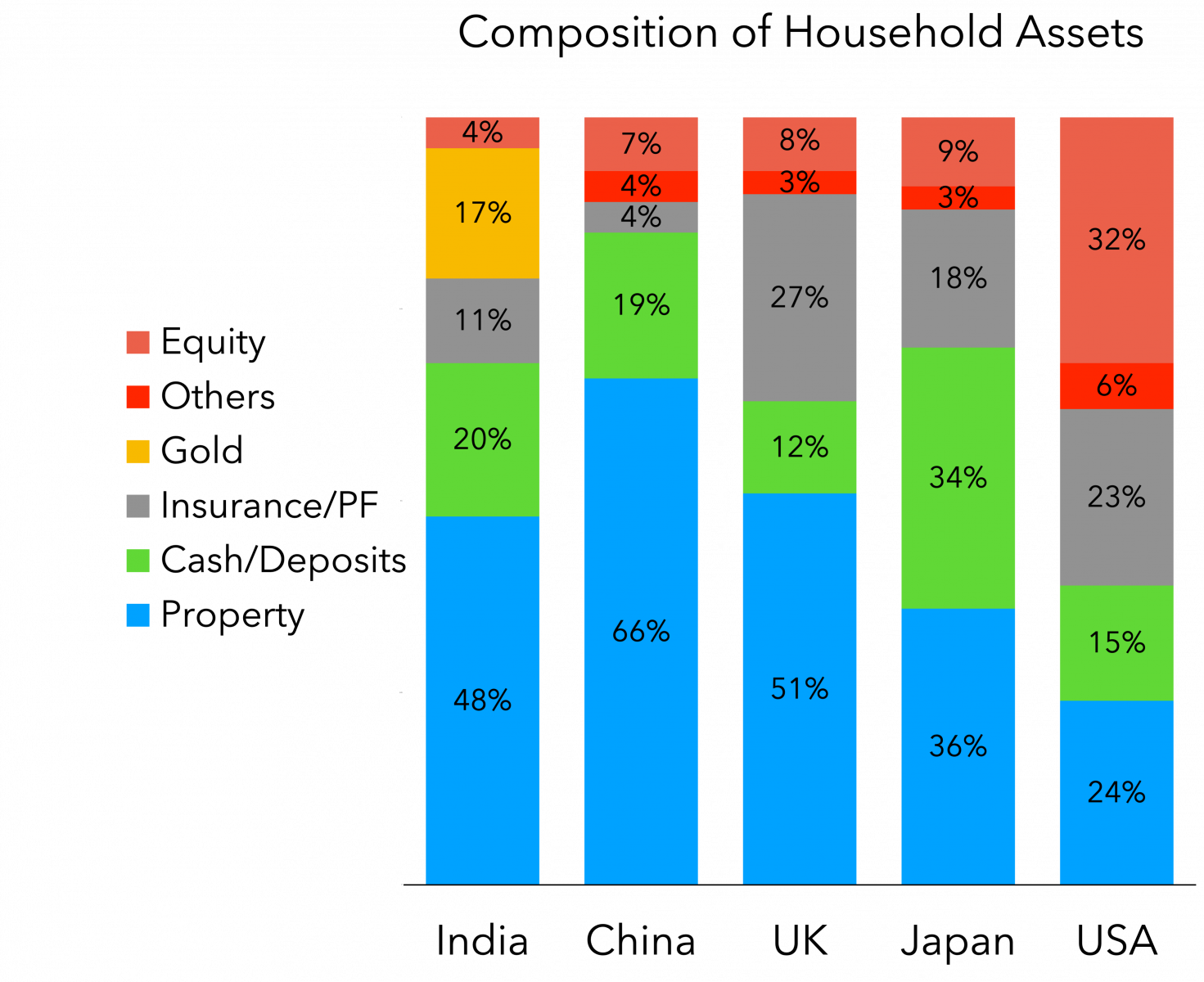

When it comes to India, the composition of household assets as of December 2020 is largely physical, like – Property, Gold and Cash (83% of total assets). Financial assets like Insurance and equity investments are merely 11% and 4% respectively. As opposed to equity investments as a % of household assets in other developed countries like China, UK, Japan, and US are significantly higher at 7%, 8%, 9% and 32% respectively.

The wealth management industry in India is quite small plagued by a lack of education, awareness, and willingness to invest in equity investments. India faces a lack of legal and disposable income. Out of the 1.3BN population in India, only 58MM users file taxes (needed to invest in financial assets like equities) and about 43MM users earn below $7,000/year. Bank of America in a report estimates that the market size of the wealth management industry is merely $8BN with a target user base of 60MM users (<5% of the population).

While the market size remains small, India is seeing a massive increase in adoption and growth led by newer and younger users.

The below table explains it all. A record number of new accounts opened and active traders i.e., individuals that have made at least one transaction in the past 12 months.

|

|

2019 |

2020 |

% Increase |

|

New Accounts |

4MM |

10.5MM |

162% |

|

Active Traders |

9.5MM |

17MM |

79% |

Source: Business Standard, Mint

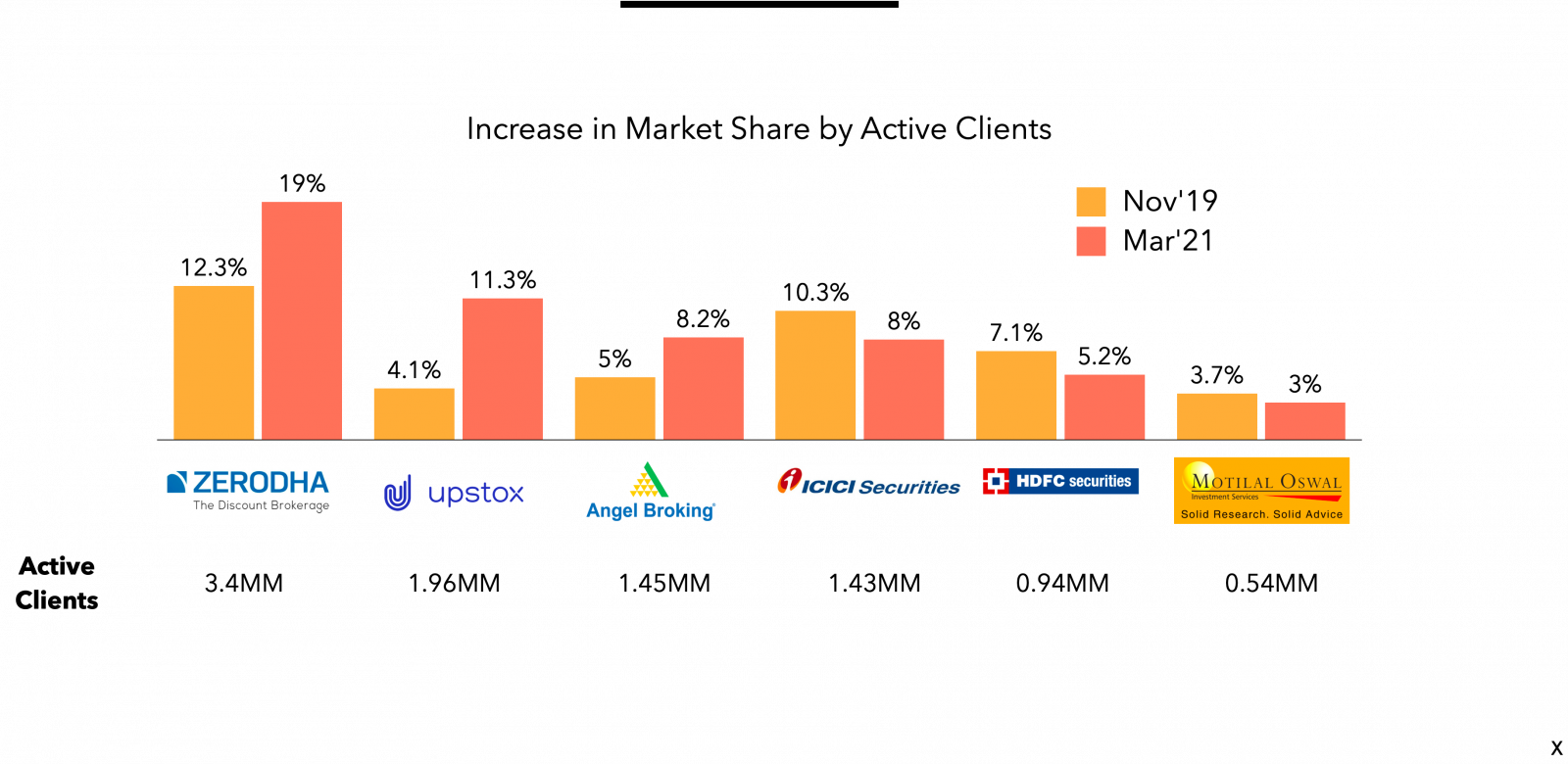

The beneficiaries of this new surge of users are the digital first discount brokers that are taking market share away from incumbents. In 2015, there were zero discount brokers in the top 10 brokers by size. In 2021, we have Zerodha, Upstox, Angel Broking and Groww in the top 10 list.

Some of the key reasons for the rise in digital discount brokers are convenience, millennial friendly brand - increasing investments in content and lower costs when compared to incumbents.

Convenience – Since 2016, the rise of internet and mobile adoption has skyrocketed leading to the users preferring to trade on mobile as opposed to make trades on desktop or via phone call to brokers. According to Zerodha, over 75+ of the trades are now made on mobile as opposed to 80% being made on desktop a few years ago. These digital platforms have invested in technology and apps to provide users ease in KYC to onboarding to adequate investing tools to portfolio management.

Millennial brand – According to Zerodha, average age of users has gone from 32 years pre-covid to 26 years post-covid. The increasing younger population prefers superior apps and brand resemblance provided by digital first discount brokers as opposed to the low convenience and brand resemblance of incumbents.

Content – Platforms like Zerodha, Groww and Upstox are seeing record growth in the sign-up of first-time investors. One of the leading reasons for first time users signing up is these platforms are increasingly sharing best practices and education content via YouTube channels or on their own platform (Zerodha Varsity) to educate the customer on how, why, where and what to invest in.

Lower Cost – Bank (incumbent) brokers often charge traditional fee to customers 0.3%-0.5% per order for equity and Rs. 70 -300/ lot on option orders whereas discount brokers charge customers a fixed fee plan that charges a maximum of Rs. 20 on option and intraday orders and no charges on equity delivery orders.

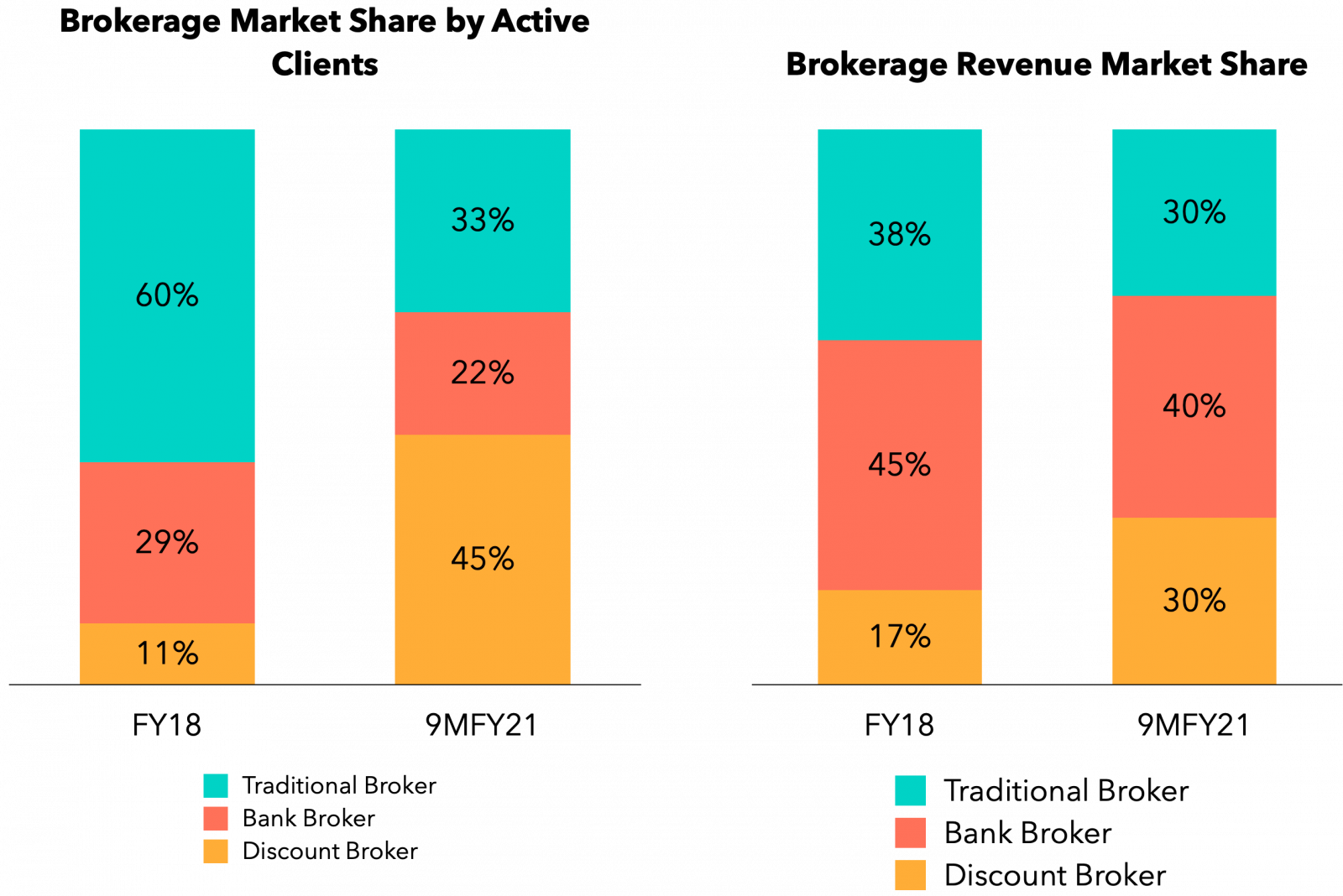

While the digital platforms are gaining users, incumbents still hold majority of the revenues.

The difference in traditional plan and modern fixed fee plan by brokerages have led to higher number of users for discount brokers (45% of the industry users) and higher monetization for traditional and bank brokers (70% of the industry revenues). According to the AMFI, ARPU for bank owned brokers (ICICI sec, HDFC sec) is roughly Rs. 10,000-12,000 as they use a traditional revenue model, provide value added services like advisory for their higher net worth clients whereas the discount brokers have an ARPU of Rs. 4,000-8,000 due to the fixed fee model, no advisory services to their lower net worth customer.

Source: Outlook India

While the bank brokers today enjoy leadership on a revenue basis, it’s a matter of time before these discount brokers surpass them with increasing clients and higher number of trades by clients on the platform.

Additionally, the trail commissions that banks enjoyed from distributing various types of regular mutual funds has been declining in the past few years. Discount brokers have provided an option to invest in direct mutual funds where the distributors (in this case the discount brokers) don’t make any money on commissions. As of 2017, distributors made $1.2BN in fees on trail commissions and now direct plans as % of mutual fund AUM accounts for 20% as of 2021 up from 10% in 2017. The share of direct plans is expected to scale aggressively in the coming years, thus further impacting overall commissions.

The new allure of the AMC license with a focus on passive funds

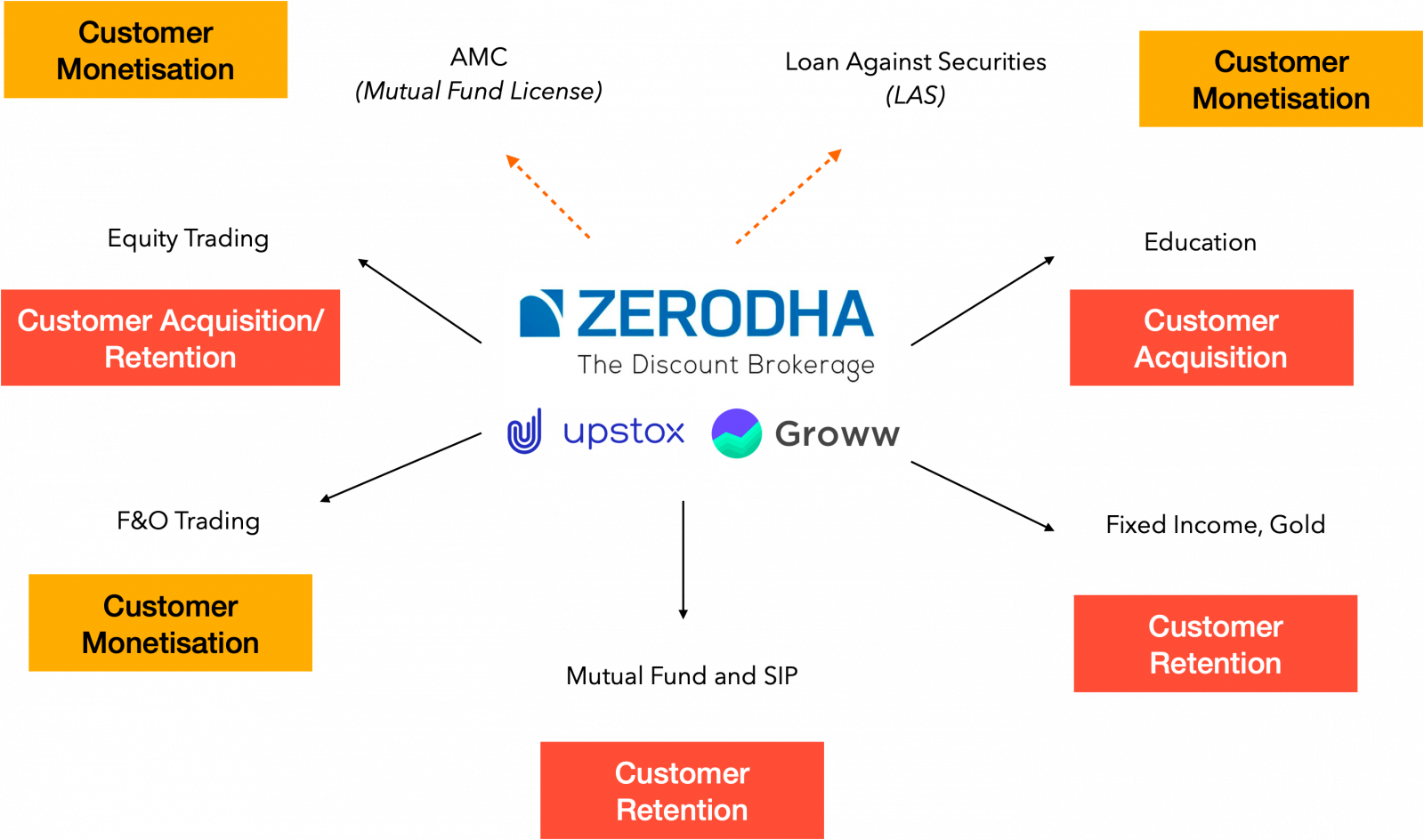

With little to no monetization through equity delivery, distribution of mutual funds, bonds, and gold investments, the discount brokers are going after AMC licenses which allows the platform to manufacture active and passive products (Mutual Funds, ETFs) funds in order to boost monetization. Groww, Zerodha, Angel Broking, Navi and other platforms have already applied or acquired an AMC license. This AMC license gives the platform the ability to then monetize up to 2% of the funds AUM.

Interestingly, the discount brokers are going after passive funds like ETFs and index funds with a vision of becoming the Vanguard of India. Currently, less than 2% of the Mutual fund AUM is in ETFs and Index funds (US passive funds have 50%+ share). The large fund houses have been focused on active funds due to the higher monetization opportunity when compared to passive funds (1-2% fees on active funds and 0.05-0.2% in passive funds). With most of the active funds unable to beat the indices like Nifty50 and Sensex, it begs the question as to why not just invest in passive funds. Navi has already launched their “Navi Nifty 50 Index Fund” and Zerodha wants to launch more passive funds as they want to make investing simpler and directed at defined use cases like funds focused on retirement. With increasing consumer education and new ETF products, we can expect to see a significant rise in ETF as a % of Mutual Fund AUM.

The rise in new products and Alternative Investment class

In equities, we are seeing Smallcase that lets individuals invest in a concentrated basket of stocks managed by investment professionals across various themes or strategies at a minimum of Rs.500. For example – if an individual is bullish on electric vehicles, a Smallcase is available that invests in the companies that are enabling the rise of electric vehicles. Earlier, such a service was only available for the high-net-worth investors via Portfolio Management Services (PMS) where the minimum investment is Rs. 50 Lakhs ($66,000).

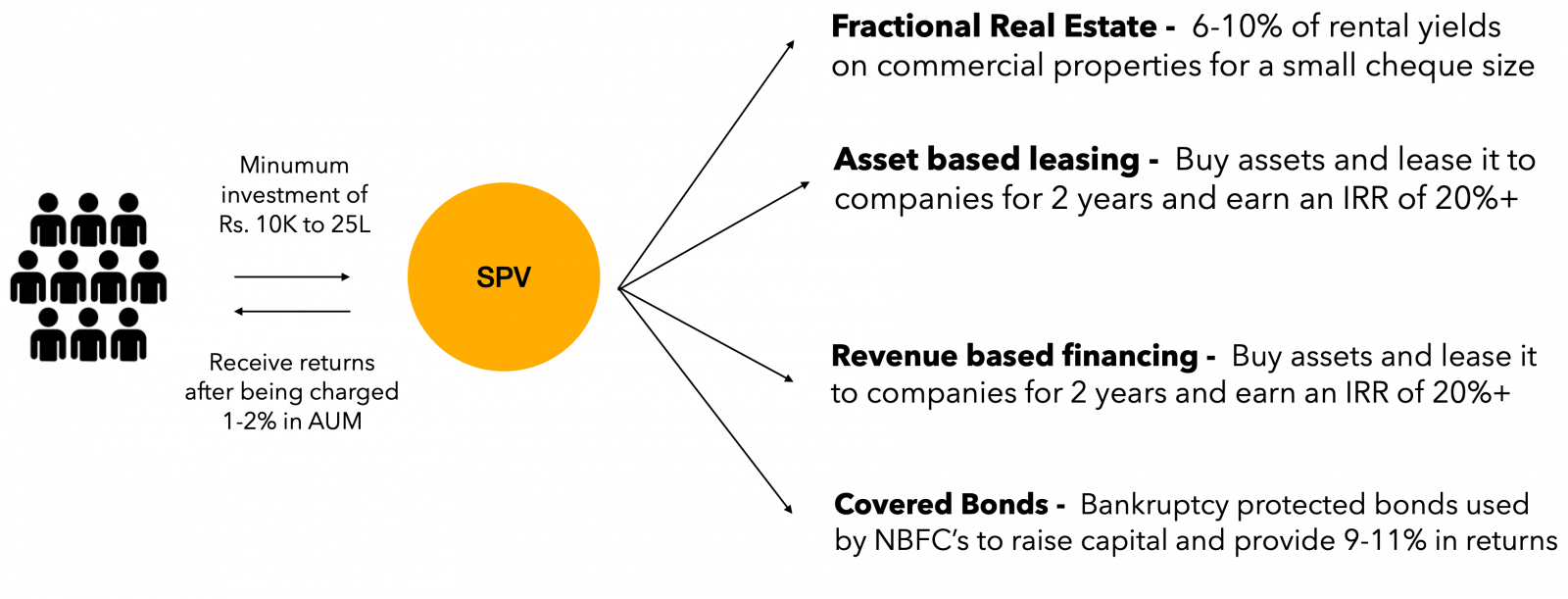

Outside of equities, we are seeing more and more innovation in alternative investments where companies are democratizing access for retail investors that were earlier available only to the institutions and high net worth individuals. Products in this range that we have seen are Fractional Commercial Real Estate provided by Propshare and Strata, and various debt products like Asset based Lending provided by Grip Invest, Revenue based Financing provided by Klub and Covered Bonds provided by Wint Wealth.

Democratizing investing in these assets is quite exciting especially for retail investors who have an opportunity to diversify their investments across asset classes from equities to real estate and debt products. Opportunities which did were not previously accessible due to the requirement of high ticket size. The companies operating in this segment charge 1-2% of AUM to investors for managing their assets and providing higher returns. While all of this is exciting, there remains risk as these products are new and remain to be seen how it will be regulated at scale. Time and time again, we have seen SEBI taking protective measures for retail investors. If one of these alternative investment products goes bust, we can expect some strict measures. While there remains a risk these products are operating in a large TAM and democratizing access to retail investors and we are looking at this sector closely.

Potential of Social investing in India

One of the themes that we have often talked about at Lightbox is that every industry as they move from analog to digital they will also move from individual to social.

“Just as every industry makes the crucial transition from analog to digital, nearly every category of companies will eventually make the transition from single-player to multiplayer, from company-driven to community-driven, from individual to social”

We believe that retail investing is highly social influenced. Retail investors are often learning, finding, and understanding companies by talking to friends on WhatsApp, being in investment groups on Telegram, reading about them on twitter or watching content about them on YouTube. Moreover, according to a survey 38% of the Gen-Z population is learning about personal finance on Tiktok, YouTube and Reddit. So what could a social platform for them look like?

Globally, we have seen social investing in the form of eToro, Public.com and Common Stock emerge where the retail investors can copy trades from people who they follow and can invest based on their thesis in stocks. While that’s gaining a lot of traction globally it is currently illegal in India to do so. Hence, we will need some first principles thinking from start-ups to build a social investing platform in India and we at Lightbox are keenly looking into this space.

Conclusion

The years 2020 and 2021 have undoubtedly been a great time for all kinds of investing apps. We have seen the dominance of discount brokerages in India that are gaining market shares and the highest number of new retail investors opening investing accounts. While, much of it can be attributed to the bull market and higher disposable income, this period has definitely witnessed the emergence of new behavior of investing across equities, options, debt and gold products. We believe that the innovation for retail investors is just getting started from democratization of access to new asset classes that were earlier available only to the institutions and HNIs, emergence of ETFs and passive funds that were ignored by large fund houses and lastly potential rise of advisory and social led investing in the coming decade. We are excited to see the evolution of the markets and are actively looking to partner with innovative companies in the space.

If you believe you are building something we would find interesting, please write to us at hello@lightbox.vc.