In the past 20 years, we have seen physical goods (books, clothes, accessories) and services (travel, entertainment) which were mostly being sold offline, now aggressively being sold online. Banking is one of the last few bastions of services still being delivered offline, however, we are now beginning to see the transition to online happen here as well.

Over the past year we have seen the emergence of neo banks - digital only banks that provide top notch banking experiences via an app and at costs far lower than offline banks. On this promise, we have seen neo banking become one of the hottest sectors in the startup ecosystem globally. According to Accenture, the total funding globally in digital banks has been around $5.2BN in 2019 alone (3x more than 2018). In India, according to Mint, $116MM in funding has been given to digital banks in 2019, most of which are in pre-launch or beta stage.

Through this post we hope to explore the evolution of the digital banking space globally and lessons we can draw upon for the Indian upstarts in this space.

Before we get into that we would like to clarify the two terms - Neo Banks and Challenger Banks that are often used interchangeably in the industry. So to differentiate between them for this discussion we have used this framework-Challenger Banks are digital only banks that have their own banking licenses, Europe and Brazil have challenger banks. Neo Banks are digital only banks that sit on licensed partner banks (i.e. they don’t have a banking license). US and India primarily have Neo Banks due to regulation hurdles.

First stop – United Kingdom, the place where the digital bank phenomenon began:

It all started after the Global Financial Crisis in 2008, which highlighted a structural problem in the way banks were operating at the time. Reacting to the crisis, the Bank of England initiated changes in the banking system quickly. First it decided that the banking sector could no longer be dominated by five big banks. This was the first time in 100 years that the authorities decided to give out a new banking license. Furthermore, the authorities in 2014, decided to boost competition in the financial services and it did so by loosening the red tape for opening a bank in the UK. The authorities received about 29 applications for new banking licenses of which a few of them were for digital only banks.

Monzo, a UK domiciled challenger bank born of the liberalization of the banking sector, has scaled to becoming amongst the most popular digital only bank in Europe. It has done so by focusing on solving real customer problems via elegant product led solutions. Monzo has attracted over 4MM users since inception. Today, 1 in 20 adults in the UK bank with Monzo, a remarkable feat achieved in three years.

Their journey began with easing the process of opening a bank account. Through this move they ensured that people wouldn’t have to wait in long lines at a bank, fill out 20 manual pages for KYC, or skip work to go to a bank to open a bank account. According to a Reuters report, traditional banks, in the UK, took 32 days on average to onboard a customer in 2017. In contrast, Monzo lets customers open a bank account in 5 minutes by just taking a selfie with a government issued ID and sends them an attractive coral debit card in less than 48 hours. Many virtual banks like Monzo have now taken the time to build a mobile first customer-centric banking.

In Europe, it is commonplace for people to travel across borders often for work or holiday. Monzo and other neo banks do not charge customers additional fees for making transactions during international travel, unlike traditional banks like Barclays that levy a 3% fee on every international transaction.

Monzo also lets customers know how much they have spent via real time notifications while nudging them on how they can save money. On the other hand, until recently, customers of legacy banks were only able to view their daily expenditure belatedly after their billing cycle.

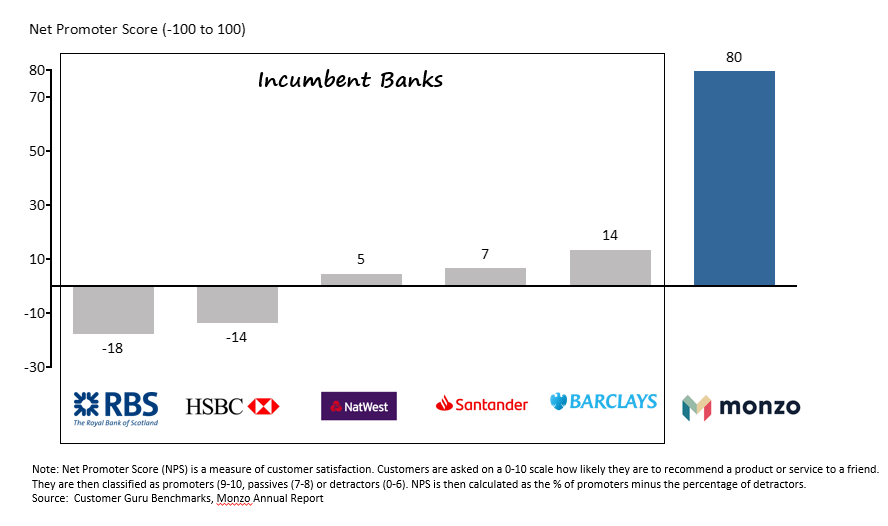

Compared to the big banks, digital only banks like Monzo have a much higher NPS. Source: HBS

The flip side

While Monzo has gained early success, they’ve had a fair share of issues. One of the key issues being not used as a primary account by a customer. According to Quartz, Monzo has 4MM customers with $568MM in total deposits (Avg. $142/account) whereas Barclays has 15MM customers with $253BN in total deposits (Avg. $16,700/account).

In terms of monetization, Monzo currently earns the majority of its money through interchange fees, typically borne by merchants, and plans to introduce subscription banking with premium benefits (unique model in banking) and lending (it will have a cost of funds advantage due to its banking license). Given the many challenges with the current banking system in the UK, Monzo seems primed to make a massive dent in the banking economy.

Second stop – United States

In 2018, 78% of workers lived paycheck to paycheck and 15% of Americans struggled with a $400 emergency payment when in need. Income growth in the US has laggedthe growth seen inexpenses such as healthcare, education, and housing for the past 25 years. To add to this, banking is expensive.

The US banks are notorious for charging all sorts of additional fees. The most expensive being overdraft fees. If a transaction made is more than the available balance, banks approve the transaction, but charge customers an overdraft fee of $35 . On average Americans pay $250 in overdrafts every year. In 2017, this led to big banks making $34BN in profits just through overdraft fees.

Furthermore, the banking infrastructure in the US is amongst the most archaic in the world. They have no equivalent to UPI, IMPS or NEFT, services we take for granted in India. In fact, they operate on the ACH (Automated Clearing House) system where if a company pays their employees on a Tuesday night the money will only be available to the employee to use on Friday. (Takes 3 days!)

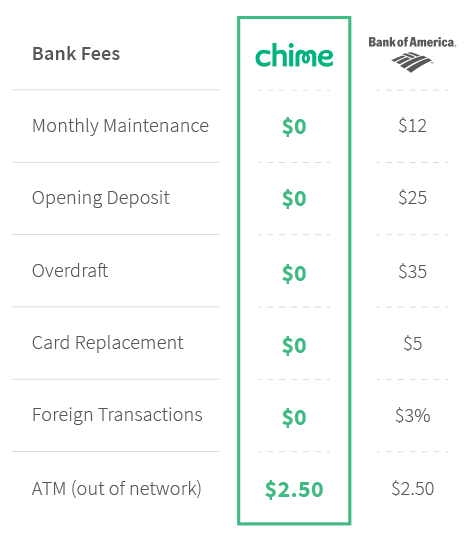

In comparison, neo banks like Chime reduce the hassle for customers when it comes to managing their finances. Chime targets customers who earn less than $75,000/year. They provide zero balance accounts, waive off all fees that a big bank may charge, and include free overdrafts up to a certain limit. Chime also provides early payday where they release salaries to their customers the day after their employers initiate the transfer instead of waiting for the standard three days that too at no additional cost. Early payday is a massive relief for customers living paycheck to paycheck and has increased their willingness to use Chime as their primary account. The company has been able to win this market with close to 6.5MM customers in Nov’19.

The reason big banks charge these absurd fees is because of their high operating cost model, where the unit economics don’t work if the big banks take away banking fees as seen in the image below.

Source: Chime

Those days where banks make money when you make a mistake are coming to an end, the new digital banks are trying to show us that money doesn’t need to be made by doing wrong by the customer.

When it comes to monetization, Chime is taking advantage of a regulation rolled out on account of the Durbin Amendment in 2011. In this amendment, banks with more than $10BN in assets can charge a maximum of 0.05% + $0.21 in interchange fees (borne by merchants) on a debit card down from 1.19% + $0.10 prior, affecting the revenues of the big banks massively. While banks below $10BN in assets can charge 10-20 times higher interchange fees on a debit card. As Chime sits on a partner bank that has less than $10BN in assets, its interchange revenues for 2019 is estimated at over $200MM.

Next, Brazil where Challenger Banks helped reach customers that were earlier unbanked :

In Brazil, one in three locals don’t have a bank account. Opening a bank account can take days if not months. The founder of NuBank, himself tells the story of how painful and bureaucratic opening a bank in Brazil was which inspired him to start NuBank.

One in three adults Brazilians don’t have a bank account. The Net Interest Margin (Interest on loans minus interest on deposits) in Brazil is 40%. It’s a horrendous rate as the world average including India is about 8%.

The top five big banks control 85% of the market as a result have little incentive to innovate.

This is where NuBank became a light in this darkness. Opening bank accounts was hassle free without going to the branch and credit cards rates were cheaper than big banks. Their value proposition was so strong that about 80% of the new customer sign ups were through word of mouth. It now has 15MM users, highest globally among digital only banks.

In terms of monetization, Nubank earns revenues through interest on credit cards. As Nubank, is a licensed partner it receives the same cost of funds advantage that other big banks in Brazil do.

The BIG advantage: Cost structures for Digital Banks look like those of social networks rather than traditional banks

One of the advantages that all digital banks mentioned above have is the cost structure. Traditional banks have massive costs in terms of real estate (bank branches) and headcount i.e employees. The savings for digital banks from here are returned to the customers by providing better interest rates on savings and getting rid of absurd fees all while ensuring a superior customer experience.

|

|

Customers per employee |

Employee wages per customer |

|

Traditional Banks |

250 |

$164 |

|

Neo Banks |

5,815 |

$17 |

|

|

70,250 |

$3 |

Source: a16z

To summarize Neo Banking

Last stop, Neo banking in India:

India has been at the forefront of building cutting edge financial infrastructure and ensuring financial inclusion for all. Products like Unified Payment Infrastructure (UPI) have democratized access to digital payments by making such payments easier, faster and cheaper. UPI completed 1.3BN transaction in Feb 2020 alone, higher than the number of debit and credit card transactions in India combined. It has been such a success that Google has recommended that the US Federal Reserve consider it for faster digital payments in the US.

Today, more than 80% of the citizens in India have a bank account, higher than the world average of 67%.

All of this has been possible due to a combined effort by various stakeholders across the ecosystem.

Neo banking would seem like the perfect platform to take advantage of the advancements in our banking infrastructure. However, from, what we have seen so far it appears that Neo banks are nothing but superior UX layers that sit on top of incumbent banks. Besides providing a better digital experience to access existing banking services they do not solve a vast customer pain point. A lack of clarity around regulations governing digital banks has meant that existing banks have been silent spectators as they wait to see how neo banks evolve. These incumbents have been happy to partner with digital upstarts as these partnerships help expand their base of active accounts – a metric that drives valuation. With no license to operate independently it remains to be seen how neo banks will be able to find scalable monetization opportunities beyond lending.

While there has been talk of a regulatory framework to manage digital banks little has moved on the ground. The biggest traditional banks in the country are a part of the regulatory body that will dictate how the digital banking policy will evolve. Which means you have a situation where the incumbents may be using the digital upstarts to learn about the space and eventually regulate them out. There are some startups that could navigate these issues and emerge triumphant. But, to find a clear winner in the plethora of neo banking startups is difficult due to minimal or no product differentiation among them. We expect the best outcome for the triumphant upstart will be an acquisition by an incumbent themselves.

While digital banks globally have been giving incumbent banks a run for their money, like Monzo to Barclays or Chime to Bank of America or Nubank to Banco do brasil, India’s neo banks will have a massive challenge to do so. It needs first principle thinking, differentiated products and solutions as the problems and business models that apply globally don’t apply in India.

We at Lightbox, like to back companies with a differentiated product that can dominate market share in a particular sector or sub-sector. If you think you’re going after a big enough problem with a differentiated product and strategy, we would love to talk to you.